In part #1, we understood why food delivery businesses have been losing money by analyzing their unit economics. If you haven’t read that as yet, I recommend you to do so before moving on.

Let’s now look at what these businesses can do to improve margins.

The play for margins

Let's have a look at some ways in which food-delivery businesses can improve margins and achieve business-market fit:

Option #1 - Pinch the delivery executive

Delivery platforms decide the delivery fee and a % of that is given to the delivery agent. Therefore, one way to increase margins is to adjust the delivery fee to maximize the margin for the platform at the cost of the delivery agent.

Option #2 - Pinch the restaurant

Food delivery platforms charge restaurants a commission - called the "take rate" - on every order placed via them. Therefore, another way to increase margins is to increase this commission %.

Now, food aggregators are dependent on these stakeholders for day-to-day operations and messing with them isn’t exactly a wise thing to do. So what's a better solution?

Option #3 - Change the value chain

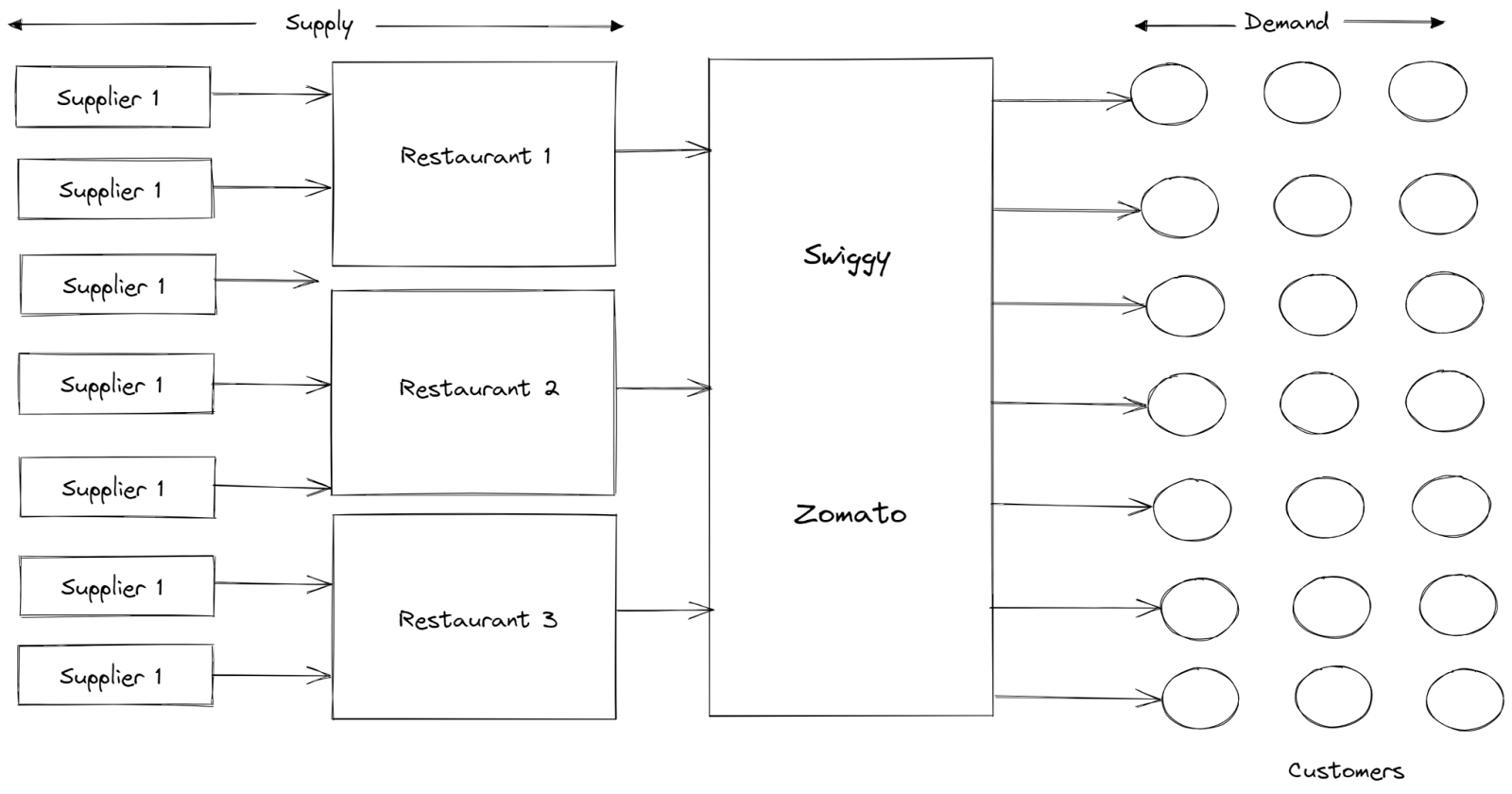

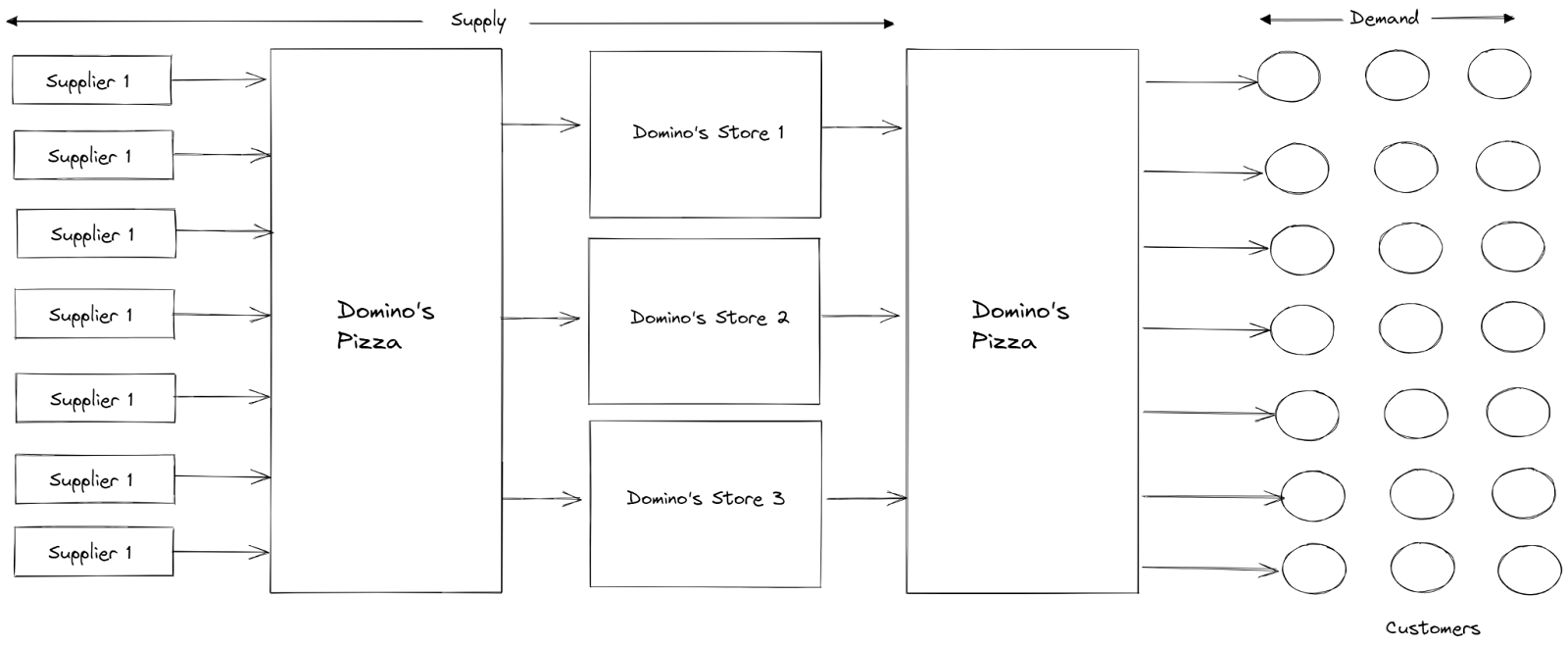

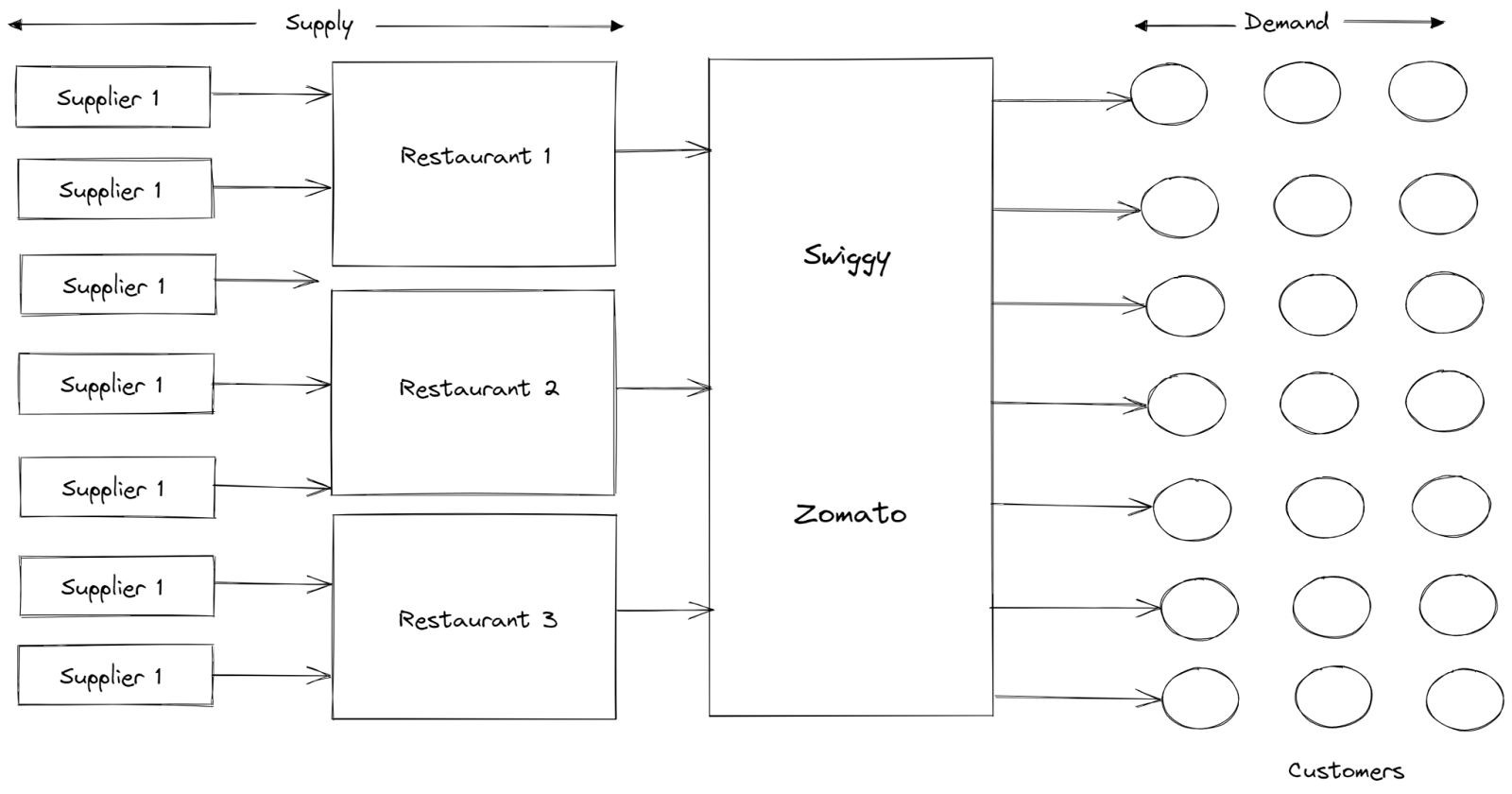

To better understand this proposition, let's see the differences in the value chain of food aggregators & Dominos.

Food delivery platforms are aggregators of demand. They stand between the restaurants and their customers.

Contrast this with Domino's' value chain.

Similar to food delivery apps, Domino's aggregates demand. But unlike food delivery platforms, Domino's has control over the supply side too. It negotiates with suppliers and sells raw materials to its franchise stores. This translates to lower costs and lower price volatilities in raw materials1 since Domino's has high bargaining power against the suppliers.

Food aggregators are adopting this strategy of vertical integration with the supply side through cloud kitchens. It can be best explained by understanding Casey Winter's "3 stages of a Marketplace"2 -

Stage 1: Aggregate consumer demand, onboard restaurants (supply), and connect the two

Stage 2: Own the delivery network, thus bringing the service to the customer. This enables food delivery platforms to identify popular dishes, preferences, ordering patterns

Stage 3: Own supply by creating a cloud kitchen based on learnings captured from stage 2

HBS Professor Sangeet Paul Chaudhary sums it up best - “Restaurants take the risk of starting up. Delivery platforms learn from them and build more robust demand models than any individual restaurant ever could.”

Cloud kitchens benefit from:

Lower rents

Lower delivery costs as kitchens can be located closer to demand hotspots

Lower costs of waste as demand can be predicted better

This is essentially a 'platform-as-producer'3 play where the platform competes with producers in its ecosystem.

Swiggy and Zomato are both playing in this segment. Swiggy has established 1,000 cloud kitchens4 for its restaurant partners, invested in more than a million square feet of real estate space across 14 cities in the country, and spent a total of $24.5 million in its cloud kitchens business that it calls Swiggy Access. Zomato invested $15Mn5 in Loyal Hospitality, a company that offers a platform to restaurant partners for planned exponential expansions without investments, and will be the sole delivery partner for the kitchens covered under the programme.

However, cloud kitchens come with their own set of problems. Single-brand cloud kitchens have limited scalability. In order to achieve meaningful scale, cloud kitchens need to have multiple brands under their umbrella (Rebel Foods, the market leader, operates 320 kitchens6 with 20 brands7). However, this results in a vicious cycle - owning multiple brands means investing in physical capital in the form of additional kitchen space (which is difficult to scale) and an increase in marketing expenditure - thus driving down profitability. Increasing prices isn’t an option either because customers expect lower prices because of limited brand recall and recognition. It’s no wonder that cloud kitchens are no longer an area of focus for VCs8. The pandemic has only added problems. Consumers9 prefer to order online from a well-known brand name due to health and hygiene concerns, even if it is slightly more expensive. Due to this behavior, Swiggy had to shut-down three-fourths10 of their cloud kitchens and Zomato exited the partnership with Loyal Hospitality11.

What does the future look like?

One thing seems to be clear: it’s difficult for food delivery as a standalone business to survive. When the capital dies down, the problematic dynamics of the industry will come to light, and people will realize how incredibly inefficient the business model is.

Let’s have a look at the value chain to explore what the duopoly can do to turn profitable -

First, the supply side -

Adopt a Domino’s-type model as explained above. Essentially, negotiate with suppliers to procure fresh and quality produce and then deliver it to restaurants. This is exactly what Zomato is doing with Hyperpure. Hyperpure allows restaurants to buy everything from vegetables, fruits, poultry, groceries, meats, seafood to dairy and beverages from Zomato. It allows Zomato to widen it’s addressable market considerably, given that India currently has 70 Lakh restaurants and the bigger market opportunity comes from the 2.3 Cr restaurants in the unorganized segment, according to FHRAI’s estimates12. The model seems to be working - over 9,00013 restaurants are reported to be availing the service. Hyperpure made Zomato Rs. 1B in revenue14, a 49% QoQ increase and Zomato plans to invest over $50M15 in it in the next 2 years.

Restaurant Staffing. One of the restaurant industry’s biggest problems remains to be of staff retention. Food delivery companies have a huge network of delivery executives, and as we’ve described above, they may be under-utilized because of infrequent demand. During non-peak hours, Zomato can divert these delivery executives to restaurants that don’t have enough labour. This is a win-win for everyone - the delivery executives earn when they don’t have deliveries to make, the restaurants get their staffing problems solved partially, and Zomato makes a neat commission

Redistribute food that would otherwise be wasted - India generates 67 million metric tonnes16 of food waste per annum which is valued at INR 92,000 crore, growing at 8-10% year on year. There isn't a lack of food, rather an ineffective redistribution of excess food. Hunger, therefore, isn’t a scarcity problem. It’s a logistics problem. And it’s one that the duopoly can solve. They can make use of their extensive restaurant and delivery network to collect & distribute the food to those who need it. This could happen by partnering with nonprofits, NGOs, and charitable organizations who pay Swiggy/Zomato for each meal distributed.

Second, the demand side -

Deliver alcohol - Food delivery apps are a convenient way to grab a meal, but what about drinks? This is one market that the duopoly hasn’t fully explored as yet. The demand for alcohol jumped due to the pandemic, and both companies were serious about the opportunity and were discussing with state governments to start operations across different cities. However, unlike food, alcohol delivery is a highly regulated market and a state subject. They faced regulatory bottlenecks, harassment of delivery staff by police, and strong resistance from alcohol retailers who often pay a very high fee for a liquor license, and view food-delivery firms as long-term competitors. Only time will tell whether the companies will be able to negotiate with the stakeholders, overcome these challenges, and deliver booze to our doorstep :)

Quick commerce - Swiggy and Zomato are both playing in this segment, and for good reason. As we've seen, these businesses struggle with making a profit and have high customer acquisition costs. This means they need customers to keep visiting them. Moreover, they have a massive delivery network that has perfected delivering food and isn't utilized to its fullest - so they can sell low-value but high-frequency order items, thus unlocking even more value for customers. This converts these platforms into utility services and solves the problems we spoke of above - low customer loyalty & underutilized drivers. However, they seem to be taking different strategies. Swiggy seems to be taking a full-stack approach. Swiggy launched its grocery delivery service, Instamart, with a commitment to deliver essentials in 15-30 minutes. Given the current growth trajectory of Instamart, it is set to reach an annualised GMV (gross merchandise value) run rate of USD 1 billion in the next three quarters, and Swiggy is investing another $700M in it. It also launched Swiggy Genie, it’s hyperlocal logistics service, which allows you to deliver or receive anything from documents to laundry. Swiggy’s COO, Vivek Sunder said that it aspires to be the “King of Convenience” by using its technology-fuelled logistics backbone to extend the convenience of food delivery to every other area. Zomato, on the other hand, is expanding via investments. It plans to invest and partner with companies to tap into growth opportunities beyond food by deploying $1 billion17 in the next 1-2 years in the quick commerce space. It’s targeting businesses that are synergistic with Zomato with the hope that over time, some of those companies will choose to merge with Zomato to continue on their growth path. It announced its entry in the grocery delivery space with it’s $100 million investment in Grofers, ecommerce logistics with it’s $75 million investment in Shiprocket, ecommerce with it’s $50 million investment in Magicpin. It is also cultivating a long-term relationship with Curefit to explore cross-selling benefits between the food and health space.

It seems the duopoly has understood that pure food delivery is a poor margin business. One in which becoming victorious is close to impossible. And therefore, for these relentless cash burning businesses, the name of the game is expanding across the value chain. That way, they build an ecosystem, in which delivery is but a part of a larger enormously positive bottomline business and infrastructure.

https://dominos.gcs-web.com/static-files/60f2485f-43c9-42d2-b660-bc4ff0b4d654

https://caseyaccidental.com/three-stages-online-marketplaces/

https://techcrunch.com/2019/11/19/swiggy-cloud-kitchen-india/

https://inc42.com/buzz/zomato-to-shut-down-its-own-cloud-kitchen-operations-under-zis-invests-15-mn-in-loyal-hospitality/

https://www.livemint.com/companies/news/rebel-foods-partners-more-third-party-brands-to-fuel-cloud-kitchen-business-11615900135246.html

https://www.business-standard.com/article/companies/from-high-street-qsr-to-cloud-kitchen-unicorn-the-rebel-foods-story-121110600639_1.html#:~:text=The%20company%20has%20over%2020,Truth%20and%20The%20Biryani%20Life.

https://indianexpress.com/article/opinion/columns/cloud-kitchen-behrouz-biryani-faasos-covid-pandemic-lockdown-zomato-swiggy-7146428/

https://indianexpress.com/article/opinion/columns/cloud-kitchen-behrouz-biryani-faasos-covid-pandemic-lockdown-zomato-swiggy-7146428/

https://www.businesstoday.in/latest/corporate/story/covid-forced-us-to-shut-three-fourths-of-cloud-kitchens-swiggy-ceo-313620-2021-11-26

https://www.businesstoday.in/latest/corporate/story/covid-forced-us-to-shut-three-fourths-of-cloud-kitchens-swiggy-ceo-313620-2021-11-26

https://timesofindia.indiatimes.com/business/india-business/70-of-hotels-restaurants-could-close-in-45-days-warns-fhrai-after-no-relief-from-govt/articleshow/75808858.cms#:~:text=India%20has%20about%2053%2C000%20hotels,body%20of%20Indian%20hospitality%20industry.

https://www.statista.com/statistics/1118331/zomato-number-of-restaurant-listings/

https://www.newindianexpress.com/business/2021/nov/12/food-delivery-company-zomato-todivest-or-shutdown-non-core-business-2382529.html

https://www.newindianexpress.com/business/2021/nov/12/food-delivery-company-zomato-todivest-or-shutdown-non-core-business-2382529.html

https://www.restaurantindia.in/article/this-hyderabad-startup-aims-to-curb-restaurant-food-waste.13101

https://in.investing.com/news/despite-increased-net-loss-zomato-to-invest-1-billion-in-startups-2959809